Headlines

- The Challenge to the Human’s Furthest Travel and a Ceasefire in the Middle East: Where Hope Meets Risk

- Trials and Survival Strategies for Shipping That Sustains the World: The Strength of “Japanese Quality” Chosen by Shippers

- ONE’s Challenge Against Mega Alliances: The Optimal Answer of “Ease of Use” That Turns Smaller Scale into a Strength

- Middle East Tensions Hit Hard! Fuel Shortages at Main Ports to Drive Short-Term Freight Increases

- A Lifeline for SMEs? ONE’s Card Payment Solution Eases Cash Flow and Administrative Burdens

- Tank Containers as a Solution to the Logistics Crisis: Will COSCO Expand Their Business by Owned Tank Containers?

- Newly Built Container Information March 2026: Carriers Enter a “Scramble for Containers”

The Challenge to the Human’s Furthest Travel and a Ceasefire in the Middle East: Where Hope Meets Risk

On the afternoon of April 1 (Wed), the U.S. National Aeronautics and Space Administration (NASA) launched the crewed spacecraft Orion carrying four astronauts to orbit the Moon. On the second day of the mission, Artemis II, the spacecraft entered lunar orbit, and at around 7:00 PM on April 6 (Mon), it reached the far side of the Moon, marking the farthest distance ever traveled by humans—406,771 km (248,655 miles) from Earth. After completing its 10-day mission, it is scheduled to return to the waters off California on the night of April 10 (Fri). The United States’ boundless pursuit of space exploration continues to inspire people around the world with a sense of romance and ambition.

At the same time, we are reminded of the harsh reality of the conflict involving Iran—desperately resisting the blockade of the Strait of Hormuz—and Israel and the United States. However, we take some relief in the announcement made on April 7 (U.S. Eastern Time) that both sides have agreed to a “two-week ceasefire,” albeit with slight differences in interpretation. We sincerely hope that the conflict will be resolved amicably through dialogue between the parties.

Trials and Survival Strategies for Shipping That Sustains the World: The Strength of “Japanese Quality” Chosen by Shippers

Currently, maritime transport accounts for approximately 80–90% of global cargo transportation by volume. Since the 1960s, the revolution brought about by containerization has made an immeasurable contribution to global economic development.

Global supply chains have been significantly impacted by a series of disruptions, including the COVID-19 pandemic, the blockage of the Suez Canal, transit restrictions at the Panama Canal due to drought, labor strikes on the U.S. West Coast, and most recently, the closure of the Strait of Hormuz. Container shipping lines, which play a central role in these supply chains, are consequently bearing an increasingly heavy burden. This is because both vessel operations and container availability are severely constrained. Shipping companies continue to deliver cargo safely to their destinations despite adverse weather, port labor strikes, equipment failures, engine troubles, port congestion, and even maritime accidents. Overcoming these challenges inevitably results in substantial cost increases.

As global logistics expanded rapidly, container shipping lines have pursued survival through consolidation and scale enlargement via mergers and acquisitions (M&A), in order to provide shippers with faster, more efficient, economical, and safer logistics solutions. It would not be an exaggeration to say that the history of container shipping is, in many ways, a history of M&A. At the same time, carriers have pursued cost reductions through the deployment of larger vessels to achieve economies of scale, thereby supporting the global supply chain as key players. By forming alliances with suitable partners, they strive to deliver better services. The success of today’s global supply chains cannot be discussed without acknowledging the tremendous efforts made by container shipping lines.

On the other hand, container shipping lines have been exposed to intense competition, and those unable to keep pace have been forced out without exception. Japan’s shipping industry has been no exception. From the six major Japanese shipping companies of the 1960s (NYK, MOL, K Line, Japan Line, YS Line, and Showa Line), the industry consolidated into three major players (NYK, MOL, and K Line) by the early 2000s. In 2017, the liner businesses of these three companies were merged to form Ocean Network Express (ONE), which established its operational base in Singapore and continues to operate today. However, its scale remains limited, currently ranking seventh among global competitors.

In 1907, during the Meiji era, Japan’s shipping capacity stood at approximately 1.07 million gross tons, accounting for about 3% of the global total and ranking sixth in the world. We hope that Japanese shipping companies will once again develop unique, high-quality services that attract global shippers. “If there is a will, there is a way.” We strongly hope they will take on the challenge—and see it through to the end.

ONE’s Challenge Against Mega Alliances: The Optimal Answer of “Ease of Use” That Turns Smaller Scale into a Strength

There are currently nine major container shipping lines worldwide. A comparison of their fleet sizes is shown below.

Post Hapag-Lloyd’s Acquisition of ZIM

| # | Carrier | Existing Fleet | Orderbook | Total Capacity |

|---|---|---|---|---|

| 1 | MSC | 7,080,958 | 2,102,992 | |

| 2 | CMA CGM | 4,081,155 | 1,909,846 | |

| 3 | Maersk | 4,602,633 | 834,770 | |

| 4 | COSCO | 3,553,514 | 1,168,612 | |

| 5 | Hapag-Lloyd *(incl. ZIM: 703,598 + 163,128) | 3,116,326 | 578,348 | |

| 6 | Evergreen | 1,938,786 | 853,113 | |

| 7 | ONEOcean Network Express | 2,050,500 | 611,304 | |

| 8 | HMM | 1,016,180 | 190,192 | |

| 9 | Yang Ming | 717,715 | 236,660 |

These nine carriers form the following four major alliances:

| # | Alliance | Member Carriers | Total Fleet |

|---|---|---|---|

| 1 | Ocean Alliance | CMA CGMCOSCOEvergreen |

|

| 2 | MSC (Standalone) | MSC |

|

| 3 | Gemini Cooperation | MaerskHapag-Lloyd (incl. ZIM) |

|

| 4 | Premier Alliance | ONEHMMYang Ming |

We sincerely hope that ONE, as part of the No. 4 Premier Alliance, will leverage its relatively smaller scale to deliver services that rival those of larger alliances, and earn a reputation among shippers as being “easy to use.”

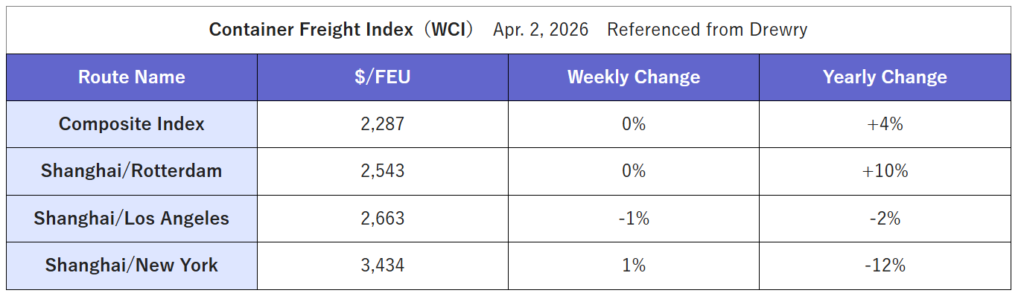

Middle East Tensions Hit Hard! Fuel Shortages at Main Ports to Drive Short-Term Freight Increases

On April 2, Drewry released its latest container shipping freight rate index.

The composite index recorded its fifth consecutive week of increase.

However, rates on the Shanghai–Los Angeles route declined both week-on-week and year-on-year. Due to the ongoing tensions in the Middle East, bunker fuel supply is reportedly tightening at major hub ports in Asia, including Singapore and China. Drewry expects that container shipping lines will introduce emergency bunker surcharges, which could push up short-term freight rates in the coming weeks.

A Lifeline for SMEs? ONE’s Card Payment Solution Eases Cash Flow and Administrative Burdens

Ocean Network Express (ONE) announced on April 7 that it has partnered with a global credit card company to launch a B2B card payment service in Japan. The service introduces online card payments for domestic transactions, with a limit of JPY 1.5 million per transaction, primarily targeting small and medium-sized shippers. This initiative is expected to significantly reduce the financial and administrative burdens faced by SMEs, particularly in terms of cash flow management and billing/settlement processes. It shortens the time and effort required for revenue collection and helps mitigate financial management risks associated with exchange rate fluctuations and interest rate changes. In addition, the service is expected to streamline ONE’s internal operations by integrating card payments with its accounting systems, thereby reducing manual reconciliation work. It also contributes to lowering the risk of delayed or uncollected payments and stabilizing the cash collection cycle. Starting from implementation in Japan, ONE is considering future expansion into overseas markets.

This initiative represents another example of ONE’s unique service offerings, and we look forward to seeing further innovative solutions from the company.

Tank Containers as a Solution to the Logistics Crisis: Will COSCO Expand Their Business by Owned Tank Containers?

According to the International Tank Container Organisation (ITCO), 28,521 new tank containers were manufactured in 2025, marking the first time since 2011 that annual production fell below 30,000 units. As of January 1, 2026, the global tank container fleet reached 899,044 units, representing a year-on-year increase of 1.93%. Most of this growth was driven by replacement demand for aging tank containers. Tank containers are increasingly used for transporting liquid cargo (mainly chemicals) and liquefied gases. Companies in this sector can generally be divided into operators, which own and operate tank containers, and leasing companies.

| # | Company Name | Fleet Size |

|---|---|---|

| 1 | Stolt Tank Containers | |

| 2 | Hoyer Group | |

| 3 | Newport | |

| 4 | Bertschi Group | |

| 5 | Intermodal Tank Transport |

| # | Company Name | Fleet Size |

|---|---|---|

| 1 | Streem Group (incl. Eurotainer & Raffles) | |

| └ Eurotainer | ||

| └ Raffles Lease | ||

| 2 | Exsif Worldwide | |

| 3 | Seaco Global | |

| 4 | CS Leasing |

In Japan as well, a shortage of truck drivers is expected to accelerate the shift from tank lorries to tank containers. Furthermore, due to their advantages in flexibility, mobility, cost efficiency, and safety, demand for tank containers is expanding beyond transportation to include storage and stockpiling applications for products such as fresh milk, alcoholic beverages, and mineral water.

COSCO Shipping has become the first shipping line in the world to own tank containers and provide liquid bulk transportation services. Previously, COSCO had established a joint venture with Germany-based VTG Tanktainer GmbH. However, following VTG’s withdrawal from the tank container logistics business, COSCO acquired a 50% stake from VTG and converted the joint venture into a wholly owned subsidiary.

Newly Built Container Information March 2026: Carriers Enter a “Scramble for Containers”

Newly built containers prices in March rose by approximately 10% month-on-month to USD 1,700 per 20ft unit, driven by increases in all raw material costs except flooring materials. Total production reached 484,608 TEU (Dry: 439,626 TEU; Reefer: 44,982 TEU). Compared to the previous month, production increased significantly by 292,826 TEU (Dry: +269,829 TEU; Reefer: +22,997 TEU), representing a 153% increase overall (Dry: +159%, Reefer: +105%).

This sharp increase is likely attributable to concerns over prolonged disruptions in the Strait of Hormuz due to the ongoing conflict involving Iran, Israel, and the United States. Containers stranded at terminals in the Persian Gulf and those waiting onboard vessels may remain idle for an extended period. As a result, shipping lines may be placing additional orders, while leasing companies may be engaging in speculative purchasing in anticipation of further container shortages and price increases.

As of the end of March, total factory inventory stood at 1,464,705 TEU (Dry: 1,411,907 TEU; Reefer: 52,798 TEU). Compared to February, total inventory decreased by 8,394 TEU (Dry: -14,407 TEU; Reefer: +6,013 TEU), representing an overall decline of 1% (Dry: -1%, Reefer: +13%).

Factory deliveries in March totaled 493,002 TEU (Dry: 454,033 TEU; Reefer: 38,969 TEU). Dry container deliveries exceeded 1.5 times the February level. This suggests that shipping lines, anticipating potential container shortages, have accelerated the uptake of previously ordered containers.