Headlines

- 1Million TEU Shortage from the Hormuz Closure!? Looming Container Shortages and Surging Freight Rates

- The Shockwaves of Trump’s Disruptive Revolution — Now!A Rare Opportunity for Japan’s Self-Reform

- 840,000 TEU Lost in the Middle East Conflict — To Sub-Saharan Africa Surges as North America Slows

- March Imports Beyond Expectations, but Demand Weakening Accelerates? Uncertain U.S. Market Outlook

- PSS Supports North America Freight Rates, but Europe Sees Limited Impact

- Newly Built Container Information – May 2026 Production Up 21%! Behind The Rush by Shipping Lines to Secure Containers

- Inspired by the Next Generation — Lessons Learned from Young People Overseas and EFI

1Million TEU Shortage from the Hormuz Closure!? Looming Container Shortages and Surging Freight Rates

Since U.S. President Donald Trump launched attacks on Iran on February 28, the Strait of Hormuz has effectively remained closed. According to the latest report by shipping research company Linerlytica, since the outbreak of the Iran conflict, only 17 non-Iranian linked container vessels, with a total carrying capacity of 127,000 TEU, have managed to sail out from the Strait of Hormuz. Meanwhile, 79 container vessels, equivalent to 312,812 TEU, have been left idle within the Persian Gulf, while an additional 28 vessels are currently being redeployed as intra-Gulf feeders.

The fact that 79 vessels equivalent to 310,000 TEU are trapped in the Persian Gulf suggests that approximately 310,000 TEU worth of empty containers are currently stranded at Gulf ports, waiting to be loaded onto onward vessels. In addition, another 310,000 TEU worth of containers are likely already en route to Gulf ports or are waiting at ports elsewhere to be transshipped onto vessels bound for the region.

If we look at the situation from that perspective, the 310,000 TEU of inactive containers trapped in the Persian Gulf could, in reality, generate container demand exceeding 1 million TEU for shipping lines, forwarders, and cargo owners trading with Gulf countries. The impact of container shortages caused by the closure of the Strait of Hormuz could therefore be immeasurable.

At the same time, the 79 idle vessels are creating a serious shortage of container ship capacity. As only a limited number of newly built container vessels have been delivered over the past two months, the market is said to be facing a severe shortage of available tonnage. As a result, charter hire rates are rising, while freight rates continue to increase due to tightening space availability.

The Shockwaves of Trump’s Disruptive Revolution — Now!A Rare Opportunity for Japan’s Self-Reform

On May 14, U.S. President Donald Trump is scheduled to meet Chinese President Xi Jinping in Beijing. As China also relies on Iranian oil for approximately 10–13% of its total imports, we sincerely hope that these two nations, whose decisions have an enormous impact on the world, will work together to achieve an immediate resolution to the Iran issue. People and nations across the globe are watching closely.

Coincidentally, during her visit to the United States on March 19, Prime Minister Sanae Takaichi reportedly told President Trump, “Donald, you are the only one who can bring peace and prosperity to the world.” Looking at today’s global leadership landscape, it may indeed be true that President Trump is the only leader capable of responding to such expectations.

There is no doubt that President Trump is an unconventional and unprecedented political leader. Internationally, through a presidential memorandum issued on January 7, 2026, he directed the withdrawal from or suspension of funding to a total of 66 international organizations and treaties, including 31 United Nations agencies and 35 non-UN-related organizations. Domestically, he has also caused major controversy through measures such as suspending federal funding for public broadcasting, freezing or reducing funding for overseas government-affiliated media outlets, and implementing large-scale cuts to foreign aid and international contributions.

Regardless of whether one agrees with his policies or not, it is difficult to imagine anyone else being able to exert such a rapid impact on long-established organizations backed by powerful vested interests. At the same time, he is forcing governments around the world to pursue self-defense and self-reform. Japan, too, must recognize that no one else will protect the country unless it protects itself. In that sense, I believe now is also an opportunity for Japan to undertake meaningful self-reform.

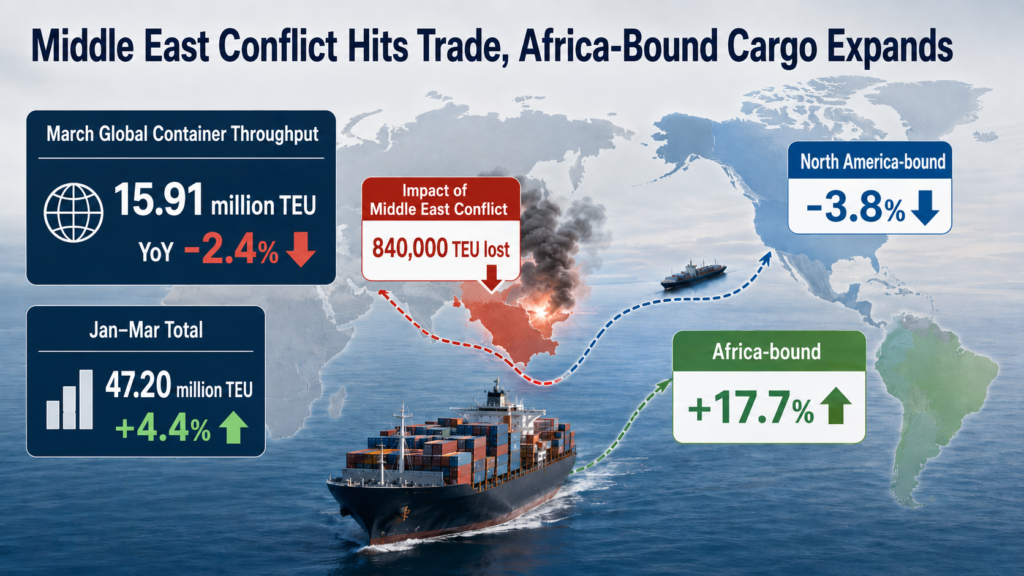

840,000 TEU Lost in the Middle East Conflict — To Sub-Saharan Africa Surges as North America Slows

According to Container Trades Statistics (CTS), which compiles global container cargo movement data, worldwide container throughput in March declined 2.4% year-on-year to 15.91 million TEU, although it increased 5.8% compared to the previous month. The deterioration in the Middle East situation was cited as the main reason for the year-on-year decline.

On the other hand, as cargo volumes in January and February had increased, total container throughput for the January–March period rose 4.4% year-on-year to 47.20 million TEU. By region, cargo movements to and from India and the Middle East, which had previously remained strong, fell sharply in March. In particular, exports from India and the Middle East declined 29% year-on-year, highlighting the impact of the worsening Middle East situation. CTS estimates that the Middle East conflict alone reduced global container cargo movements by approximately 840,000 TEU in March. The organization also expects the impact to spread more broadly over the coming months.

As for North America, container cargo volumes from the rest of the world to North America during the January–March period fell 3.8% year-on-year. CTS commented that, as long as uncertainty surrounding tariff policies continues, the contraction in cargo volumes to North America should not come as a surprise.

Meanwhile, the Sub-Saharan African region continued to perform strongly, with global container cargo volumes to Africa increasing 17.7% year-on-year during the January–March period. In particular, trade between the Far East and Africa expanded by more than 30%, leading overall growth in the region.

March Imports Beyond Expectations, but Demand Weakening Accelerates? Uncertain U.S. Market Outlook

On May 8, the National Retail Federation (NRF) and Hackett Associates released their latest actual and forecast figures for retail-related container imports at major U.S. ports. Container import volumes in March totaled 2.16 million TEU, exceeding the previous forecast by 190,000 TEU.

The April forecast was revised upward by 50,000 TEU from the previous estimate to 3.13 million TEU, although this still represented a 3.6% year-on-year decline. May is projected to increase 11.1% year-on-year to 2.17 million TEU, up 80,000 TEU from the previous forecast, while June is expected to rise 8.2% year-on-year to 2.13 million TEU, an upward revision of 30,000 TEU.

For July, imports are forecast to decline 7.8% year-on-year to 2.20 million TEU, unchanged from the previous projection. August is expected to decrease 5.5% year-on-year to 2.19 million TEU, revised upward by 10,000 TEU, while September is forecast to decline 1.3% year-on-year to 2.08 million TEU.

NRF stated that import volumes in May and June are expected to increase as a rebound from the sharp decline following the introduction of additional tariffs last year. However, the organization also believes that the downward trend in imports will likely continue, as inflationary pressures intensify amid growing uncertainty in the global economy caused by the Iran conflict.

Hackett Associates commented that container import volumes during the January–March period declined year-on-year, while future demand is also weakening. The firm added that slowing inventory accumulation and rising geopolitical tensions are making the outlook increasingly uncertain.

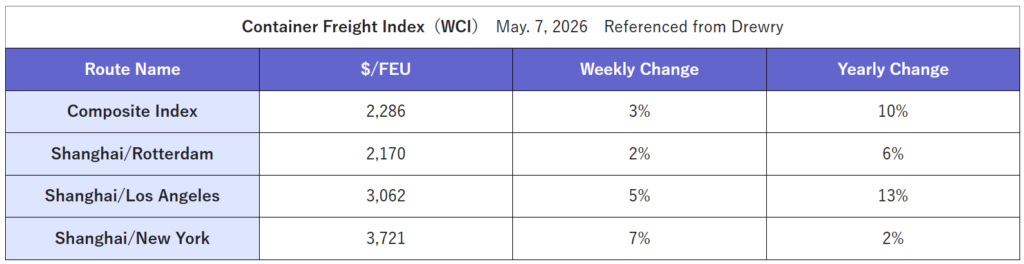

PSS Supports North America Freight Rates, but Europe Sees Limited Impact

Drewry released its latest container freight rate index on May 7.

Drewry analyzed that freight rates increased mainly due to the introduction of Peak Season Surcharges (PSS) on trans-Pacific routes. Meanwhile, for Europe-bound cargo, major container shipping lines are planning to raise short-term freight rates effective May 15. However, Drewry expects that the rate increases are unlikely to be fully realized because of weakening demand, and therefore forecasts that freight rates will remain relatively stable going forward.

Newly Built Container Information – May 2026 Production Up 21%! Behind The Rush by Shipping Lines to Secure Containers

The price of newly built containers in April rose by approximately 2.9% month-on-month, or USD 50, reaching USD 1,750 per 20ft container. The increase in flooring material prices, rather than higher steel prices, was the primary factor pushing container prices upward.

Total new container production in April reached 575,477 TEU (Dry: 532,013 TEU / Reefer: 43,464 TEU). Compared with the previous month, production increased by 90,869 TEU overall (Dry: +92,387 TEU / Reefer: -1,518 TEU). While Dry container production continued to increase, Reefer production declined. In percentage terms, total production rose 18.8% month-on-month (Dry: +21% / Reefer: -3.4%). For Dry containers, the continued impact of the Strait of Hormuz closure is believed to be a contributing factor behind the increased production.

As of the end of April, new container factory inventories stood at 1,529,015 TEU (Dry: 1,472,819 TEU / Reefer: 56,196 TEU). Compared with March, total inventory increased by 64,310 TEU (Dry: +60,912 TEU / Reefer: +3,398 TEU), representing an overall increase of 4.4% (Dry: +4.3% / Reefer: +6.4%).

Factory deliveries in April totaled 511,167 TEU (Dry: 471,101 TEU / Reefer: 40,066 TEU). It can be said that shipping lines continued taking delivery of almost the same number of containers as they ordered, in order to compensate for the expected shortage caused by the closure of the Strait of Hormuz.

Inspired by the Next Generation — Lessons Learned from Young People Overseas and EFI

Over the past two months, I had opportunities through work to meet several young people in their 20s and 30s from Italy and Spain. Through our conversations, I was deeply impressed by their sincere attitude toward work and by the genuine pleasure they seemed to feel in working with Japanese people. Perhaps this comes from their fascination with aspects of Japanese culture that differ from their own — such as Japanese anime, cuisine, and lifestyle. However, the more I came to know their personalities and character, the more strongly I felt that I would truly enjoy working together with them.

When I was young, I myself traveled abroad with little more than determination and ambition. Looking back now, I feel I am finally beginning to understand the mindset of the older and more experienced people overseas who warmly welcomed and supported me at that time.

Seeing the younger members of our company, particularly those in their 20s and 30s, demonstrating abilities beyond expectations in their work gives me great confidence and encouragement. I believe this comes from the natural affection and support that older and more experienced people feel toward younger and less experienced generations through daily communication and interaction. I am genuinely happy that I can continue to work with enthusiasm while drawing endless energy and inspiration from younger people.